Below you will find the full 64-page document titled

“Village of Piermont Financial Statements” dated May 31, 2024. That

“2024” year-date is significant.

The below 64-page report was prepared and issued by Suffern,

New York’s very own “Berard & Associates CPA’s[sic] P.C.,

Certified Public Accountants”. Judging from its date, the 64-page report is

apparently intended to correspond to a Village of Piermont “fiscal year”

commencing on May 31, 2023 and ending on May 31, 2024. Those specific dates are significant, too. “Berard & Associates” issued this 64-page report to Mayor

Bruce Tucker and the Village of Piermont, New York almost 7 months after the

close of that fiscal year, on December 16, 2024. It filtered out to all of us - slowly - thereafter.

You will next please note that nowhere on the report's cover page, is the word “DRAFT” anywhere thereupon inscribed. In fact, I cannot find the word “DRAFT” anywhere in the 64 pages of text, at least not as somehow modifying or qualifying the report as unfinished. In other words, what you find printed below is the actual document released by “Berard & Associates”, and then, released by Piermont Mayor Bruce Tucker and the Village of Piermont to the residents of Piermont. This was intended by them as an official and final communication, no matter how much they now backpedal on you once they read this Blog post and figure out how badly they messed up.

Please keep in mind that, according to its own text, the below 64-page report is based upon data and information supplied to “Berard & Associates” by Bruce Tucker and the Village of Piermont - just like any client supplies data to any tax accountant.

You will next please note that nowhere on the report's cover page, is the word “DRAFT” anywhere thereupon inscribed. In fact, I cannot find the word “DRAFT” anywhere in the 64 pages of text, at least not as somehow modifying or qualifying the report as unfinished. In other words, what you find printed below is the actual document released by “Berard & Associates”, and then, released by Piermont Mayor Bruce Tucker and the Village of Piermont to the residents of Piermont. This was intended by them as an official and final communication, no matter how much they now backpedal on you once they read this Blog post and figure out how badly they messed up.

Please keep in mind that, according to its own text, the below 64-page report is based upon data and information supplied to “Berard & Associates” by Bruce Tucker and the Village of Piermont - just like any client supplies data to any tax accountant.

Please also keep in mind that this report must have

been heavily-reviewed, vetted, and “fact-checked” by Mayor Bruce Tucker and

other perps “working” for the Village of Piermont within Piermont Village Hall.

They failed. I’ll explain.

The next thing that you, the reader, will please notice about the below text, will be the seemingly-endless series of backflip-disclaimers inscribed by “Berard & Associates” to seek to impose the real responsibility and liability on the Village of Piermont and, by transitivity, Mayor Bruce Tucker of Piermont. That’s no surprise. Having access to Piermont books and records, “Berard & Associates” already know full well that Piermont Mayor Bruce Tucker is a walking fiscal disaster as well as an environmental and aesthetic catastrophe.

Yet a further careful reading of the below “Berard & Associates” text will lead you to the conclusion that all authors and editors of this text were beyond negligent to the extreme. All are culpable.

The first stunning typographical error is found on (unnumbered) Page 5 of the “Berard & Associates” Village of Piermont Financial Statements report. The relevant passage actually reads as follows:

“Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we [that is, Berard] considered the Village of Piermont’s internal control over financial reporting (internal control) as a basis for designing audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Village of Piermont’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Village of Haverstraw’s[sic] internal control.” [Emphasis supplied].

They failed. I’ll explain.

The next thing that you, the reader, will please notice about the below text, will be the seemingly-endless series of backflip-disclaimers inscribed by “Berard & Associates” to seek to impose the real responsibility and liability on the Village of Piermont and, by transitivity, Mayor Bruce Tucker of Piermont. That’s no surprise. Having access to Piermont books and records, “Berard & Associates” already know full well that Piermont Mayor Bruce Tucker is a walking fiscal disaster as well as an environmental and aesthetic catastrophe.

Yet a further careful reading of the below “Berard & Associates” text will lead you to the conclusion that all authors and editors of this text were beyond negligent to the extreme. All are culpable.

The first stunning typographical error is found on (unnumbered) Page 5 of the “Berard & Associates” Village of Piermont Financial Statements report. The relevant passage actually reads as follows:

“Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we [that is, Berard] considered the Village of Piermont’s internal control over financial reporting (internal control) as a basis for designing audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Village of Piermont’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Village of Haverstraw’s[sic] internal control.” [Emphasis supplied].

Here is a yellow-highlighted ".jpeg" of the same passage taken directly from the “Berard & Associates” 64-page report:

That’s right. In what everybody already knew in advance was to be an historic audit report on the Village of Piermont’s farkakte financial state - one that everyone also knew would be read by hundreds if not thousands of concerned people including the good folks at the New York State Office of the State Comptroller right now in the middle of a Risk Assessment on the same Piermont books and records – the folks at Suffern-based “Berard & Associates” actually confused the Village of Piermont with the Village of Haverstraw within the space of two consecutive sentences.

This raises several questions, as follows:

1. If “Berard & Associates” is not even sure which Rockland County village they have audited and which Rockland County village they are writing about, then how can any other of the “Berard & Associates” numbers or statements within their 64-page report be considered accurate?

That’s a rhetorical question. The answer is, “They can’t”.

2. For that matter, if “Berard & Associates” simply used the Haverstraw macro template for the Piermont 64-page report, how do we know that “Berard & Associates” didn’t forget to supplant all the Haverstraw numbers with Piermont numbers in the Piermont report?

That’s also a rhetorical question. The answer is, “We don’t”.

3. Given that Mayor Bruce Tucker and his minions at Piermont Village Hall, while feigning financial competency, reviewed this 64-page “Berard & Associates” report prior to its issuance and publication, then how can any of their future representations of numbers or text ever be trusted, either? Of course, given that Mayor Bruce Tucker is the same guy who falsified thread-counts on wholesale sheets and then passed them off to garment industry buyers at a profit, then this particular question is a rhetorical question, too.

4. Should we now send “Berard & Associates” a map so that they can distinguish the difference between the Village of Piermont and the Village of Haverstraw in the future? That’s not a rhetorical question. I actually want all of you to do it.

5. To the extent that the Village of Piermont may have already paid “Berard & Associates” for this piece of dreck of a report printed below, then shouldn’t the Village of Piermont now demand and get its money back? Moreover, shouldn’t the taxpaying residents of Piermont claim that same ill-spent money back from Mayor Bruce Tucker? At least he might have the decency to pay back the taxpayers in 400-count sheets from his closet.

6. To the extent that “Berard & Associates” made this colossal gaffe because they simply lazily macro’d the text of their ponderous form boilerplate report from one client to the next, then shouldn’t Haverstraw Mayor Michael Kohut just split the cost of one single report with Piermont Mayor Bruce Tucker instead, so that Piermont and Haverstraw taxpaying residents can avoid getting hit with a double-charge? After all, Haverstraw’s document is likely pretty much the same as Piermont’s but for the Piermont-concocted numbers.

3. Given that Mayor Bruce Tucker and his minions at Piermont Village Hall, while feigning financial competency, reviewed this 64-page “Berard & Associates” report prior to its issuance and publication, then how can any of their future representations of numbers or text ever be trusted, either? Of course, given that Mayor Bruce Tucker is the same guy who falsified thread-counts on wholesale sheets and then passed them off to garment industry buyers at a profit, then this particular question is a rhetorical question, too.

4. Should we now send “Berard & Associates” a map so that they can distinguish the difference between the Village of Piermont and the Village of Haverstraw in the future? That’s not a rhetorical question. I actually want all of you to do it.

5. To the extent that the Village of Piermont may have already paid “Berard & Associates” for this piece of dreck of a report printed below, then shouldn’t the Village of Piermont now demand and get its money back? Moreover, shouldn’t the taxpaying residents of Piermont claim that same ill-spent money back from Mayor Bruce Tucker? At least he might have the decency to pay back the taxpayers in 400-count sheets from his closet.

6. To the extent that “Berard & Associates” made this colossal gaffe because they simply lazily macro’d the text of their ponderous form boilerplate report from one client to the next, then shouldn’t Haverstraw Mayor Michael Kohut just split the cost of one single report with Piermont Mayor Bruce Tucker instead, so that Piermont and Haverstraw taxpaying residents can avoid getting hit with a double-charge? After all, Haverstraw’s document is likely pretty much the same as Piermont’s but for the Piermont-concocted numbers.

You know what they say. Garbage in, garbage out.

7. Keeping in mind that when a professional renders work-product to a client as an independent contractor, the client owns the work-product and the professional retains no rights therein – do the Village of Haverstraw and Michael Kohut now have a claim against “Berard & Associates”, Bruce Tucker, and the Village of Piermont for copyright infringement? After all, “Berard & Associates”, Bruce Tucker, and the Village of Piermont just appropriated textual content from a document that Haverstraw Mayor Michael Kohut and the Village of Haverstraw likely already paid for.

8. To the extent that Haverstraw Mayor Michael Kohut and the Village of Haverstraw may have not yet released their “Berard & Associates” audit report to Haverstraw residents, do Kohut and Haverstraw now have a claim against “Berard & Associates”, Bruce Tucker, and the Village of Piermont for the premature revelation and publication of text emanating from Haverstraw’s confidential relationship with “Berard & Associates” - text which had yet to be publicly-disclosed? For that matter, how would you like it if your CPA/tax accountant revealed your name and information in text that you paid for, which he or she then sent to a different client other than you? At minimum, in a case like this, wouldn’t you expect that CPA/tax accountant to deduct some or all of his second stream of client revenue from your own bill?

Any way that you look at this FUBAR by “Berard & Associates”, Bruce Tucker, and the Village of Piermont, it’s beyond stupid. If a first-year associate at a law firm made a comparable mistake, I would expect that the associate would be fired on the spot. So, too, I hope, would a first-year working at a professional accounting firm be fired for something like this.

As if all that wasn’t bad enough, consider this next abomination found on (this time, numbered) Page 11 on the same “Berard & Associates” 64-page report prepared and issued for the Village of Piermont:

“The General Fund is the primary operating fund of the Village. At the end of the current fiscal year, the total fund balance of the General Fund was $4,038,991. This compares to a fund balance of $5,062,326 for fiscal year 2024[sic].” [Bold-face emphasis added].

7. Keeping in mind that when a professional renders work-product to a client as an independent contractor, the client owns the work-product and the professional retains no rights therein – do the Village of Haverstraw and Michael Kohut now have a claim against “Berard & Associates”, Bruce Tucker, and the Village of Piermont for copyright infringement? After all, “Berard & Associates”, Bruce Tucker, and the Village of Piermont just appropriated textual content from a document that Haverstraw Mayor Michael Kohut and the Village of Haverstraw likely already paid for.

8. To the extent that Haverstraw Mayor Michael Kohut and the Village of Haverstraw may have not yet released their “Berard & Associates” audit report to Haverstraw residents, do Kohut and Haverstraw now have a claim against “Berard & Associates”, Bruce Tucker, and the Village of Piermont for the premature revelation and publication of text emanating from Haverstraw’s confidential relationship with “Berard & Associates” - text which had yet to be publicly-disclosed? For that matter, how would you like it if your CPA/tax accountant revealed your name and information in text that you paid for, which he or she then sent to a different client other than you? At minimum, in a case like this, wouldn’t you expect that CPA/tax accountant to deduct some or all of his second stream of client revenue from your own bill?

Any way that you look at this FUBAR by “Berard & Associates”, Bruce Tucker, and the Village of Piermont, it’s beyond stupid. If a first-year associate at a law firm made a comparable mistake, I would expect that the associate would be fired on the spot. So, too, I hope, would a first-year working at a professional accounting firm be fired for something like this.

As if all that wasn’t bad enough, consider this next abomination found on (this time, numbered) Page 11 on the same “Berard & Associates” 64-page report prepared and issued for the Village of Piermont:

“The General Fund is the primary operating fund of the Village. At the end of the current fiscal year, the total fund balance of the General Fund was $4,038,991. This compares to a fund balance of $5,062,326 for fiscal year 2024[sic].” [Bold-face emphasis added].

The corresponding ".jpeg" lifted directly from the 64-page “Berard & Associates” report, is here:

So - not only does “Berard & Associates” not really

know which village they are auditing as between Piermont and Haverstraw – they don’t

even know which year they are examining or working in.

What “Berard & Associates” is trying to tell you in the above-quoted textual passage, is that Bruce Tucker’s Village of Piermont “General Fund total fund balance” diminished to the tune of about one million dollars, from the prior year to the current year examined. That should be a concern in and of itself. Then again, this Mayor Tucker is the same guy who put Village of Piermont taxpaying residents about nine million dollars in Net Position retrograde since the year he was elected, and then concealed financials year-after-year from the Village of Piermont website, from the Piermont residents, and from the NYS Comptroller's Fiscal Stress Monitoring System. The NYS Comptroller’s office confirmed to me that Bruce Tucker never made any deadline for inclusion of Piermont financials in the Fiscal Stress Monitor for the entire duration of his mayoral reign, since the commencement of his first term in 2018 forward. He was always strategically late, every year, so that Piermont voters would never detect the rapid degeneration of Piermont's fiscal health when performing any on-line search.

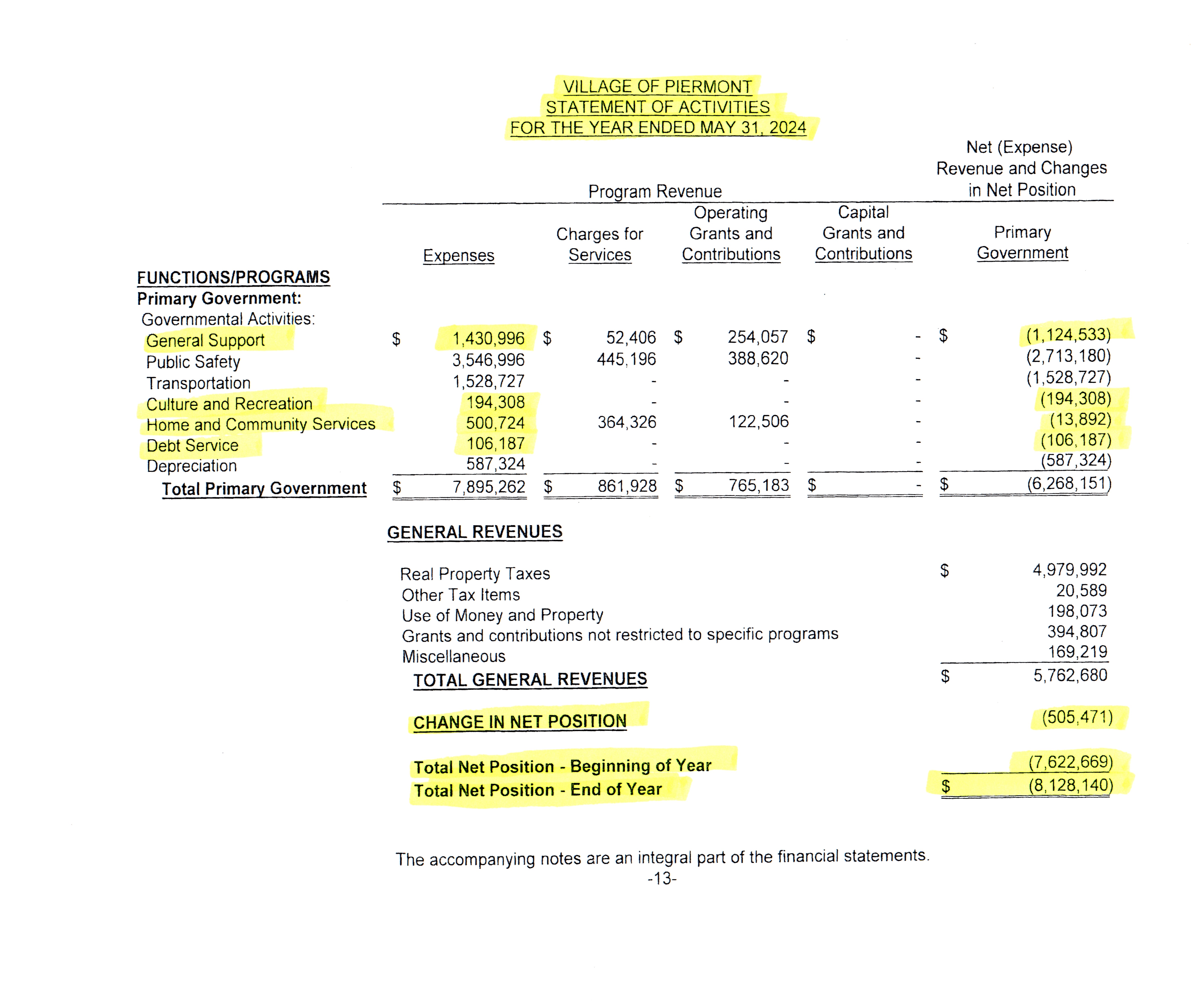

But in the above-quoted text from (numbered) Page 11 of the 64-page report, if “Berard & Associates” was trying to make the numerical comparison of a claimed $4,038,991 “balance” to a prior fiscal year as opposed to an imaginary fiscal year in futuro, then what “Berard & Associates” was really trying to do was compare "May 31, 2023-to-May 31, 2024", to "May 31, 2022-to-May 31, 2023". Therefore, in the above textual quotation, “Berard & Associates” probably meant “fiscal year 2023” as opposed to “fiscal year 2024”[sic]. Whatever they meant, it's a ludicrous mistake for an accountant to make, much less distribute for publication.

This all raises two more questions, as follows:

1. Would you want your CPA/tax accountant making this kind of inexplicable error on your own individual tax return?

2. Could this dumb blunder have actually been the CPA equivalent of a Freudian slip? In other words, pretty much this entire document is an attempt to deflect and distract the reader’s attention away from the fact that Bruce Tucker and the Village of Piermont put taxpaying residents another half million dollars into the Net Position hole since the last reckoning. Could this fudging of the year-date number be a simple reflection of the Piermont client’s instruction to its accountant, to make this 64-page report as confusing and incomprehensible as possible? Because the Berard firm and Tucker are now well on their way to that destination, if not already there.

The fact is, Bruce Tucker and his merry band of pranksters working in Piermont Village Hall are as culpable for mistakes like this, as are the folks at “Berard & Associates” apparently spinning-off common boilerplate for Piermont and Haverstraw. Chalk this up to yet another Bruce Tucker failure. Failure in the selection. Failure in the hiring. Failure in the writing. Failure in the editing. Failure in the proofreading. None of this should come as a surprise. Tucker got busted by Good Housekeeping and the Wall Street Journal as a deceiving Elizabeth, New Jersey garmento. Tucker got foreclosed-upon as a low-level second-mortgage lender in Brooklyn and Staten Island. And Tucker bailed out of the restaurant and bar business only to let his corporation get suspended and revoked. This guy marketed himself as a successful businessman when running for Piermont mayoral office. He has actually failed in every one of his pursuits.

Speaking of Bruce Tucker failures and a million dollars that abruptly goes missing, check out this next gem which “Berard & Associates”, Bruce Tucker, and the Village of Piermont sought to bury, very late in the 64-page report on its Page 47:

“C. PRIOR PERIOD [‘]ADJUSTMENT[’]

A prior period adjustment of $1,057,598 due to Ban[sic] proceeds that inadvertently reflected in the General Fund That[sic] should have been reflected in the Capital Fund to fund capital projects. This had no effect on the combined overall fund balances of the Village.” [Bold-face emphasis added].

What “Berard & Associates” is trying to tell you in the above-quoted textual passage, is that Bruce Tucker’s Village of Piermont “General Fund total fund balance” diminished to the tune of about one million dollars, from the prior year to the current year examined. That should be a concern in and of itself. Then again, this Mayor Tucker is the same guy who put Village of Piermont taxpaying residents about nine million dollars in Net Position retrograde since the year he was elected, and then concealed financials year-after-year from the Village of Piermont website, from the Piermont residents, and from the NYS Comptroller's Fiscal Stress Monitoring System. The NYS Comptroller’s office confirmed to me that Bruce Tucker never made any deadline for inclusion of Piermont financials in the Fiscal Stress Monitor for the entire duration of his mayoral reign, since the commencement of his first term in 2018 forward. He was always strategically late, every year, so that Piermont voters would never detect the rapid degeneration of Piermont's fiscal health when performing any on-line search.

But in the above-quoted text from (numbered) Page 11 of the 64-page report, if “Berard & Associates” was trying to make the numerical comparison of a claimed $4,038,991 “balance” to a prior fiscal year as opposed to an imaginary fiscal year in futuro, then what “Berard & Associates” was really trying to do was compare "May 31, 2023-to-May 31, 2024", to "May 31, 2022-to-May 31, 2023". Therefore, in the above textual quotation, “Berard & Associates” probably meant “fiscal year 2023” as opposed to “fiscal year 2024”[sic]. Whatever they meant, it's a ludicrous mistake for an accountant to make, much less distribute for publication.

This all raises two more questions, as follows:

1. Would you want your CPA/tax accountant making this kind of inexplicable error on your own individual tax return?

2. Could this dumb blunder have actually been the CPA equivalent of a Freudian slip? In other words, pretty much this entire document is an attempt to deflect and distract the reader’s attention away from the fact that Bruce Tucker and the Village of Piermont put taxpaying residents another half million dollars into the Net Position hole since the last reckoning. Could this fudging of the year-date number be a simple reflection of the Piermont client’s instruction to its accountant, to make this 64-page report as confusing and incomprehensible as possible? Because the Berard firm and Tucker are now well on their way to that destination, if not already there.

The fact is, Bruce Tucker and his merry band of pranksters working in Piermont Village Hall are as culpable for mistakes like this, as are the folks at “Berard & Associates” apparently spinning-off common boilerplate for Piermont and Haverstraw. Chalk this up to yet another Bruce Tucker failure. Failure in the selection. Failure in the hiring. Failure in the writing. Failure in the editing. Failure in the proofreading. None of this should come as a surprise. Tucker got busted by Good Housekeeping and the Wall Street Journal as a deceiving Elizabeth, New Jersey garmento. Tucker got foreclosed-upon as a low-level second-mortgage lender in Brooklyn and Staten Island. And Tucker bailed out of the restaurant and bar business only to let his corporation get suspended and revoked. This guy marketed himself as a successful businessman when running for Piermont mayoral office. He has actually failed in every one of his pursuits.

Speaking of Bruce Tucker failures and a million dollars that abruptly goes missing, check out this next gem which “Berard & Associates”, Bruce Tucker, and the Village of Piermont sought to bury, very late in the 64-page report on its Page 47:

“C. PRIOR PERIOD [‘]ADJUSTMENT[’]

A prior period adjustment of $1,057,598 due to Ban[sic] proceeds that inadvertently reflected in the General Fund That[sic] should have been reflected in the Capital Fund to fund capital projects. This had no effect on the combined overall fund balances of the Village.” [Bold-face emphasis added].

The ".jpeg" lifted directly from the report is printed here:

This raises a few more questions, as follows:

1. Who taught these clowns sentence-structure and punctuation?

2. When “Berard & Associates” says “the Village” in the text quoted above, which village is “Berard & Associates” actually talking about, this time – Haverstraw, or Piermont? Or should I wait until they receive my map in the mail before I ask them?

3. Did any of the Wall Street bond rating companies or other financial analysts already make the mistake of relying upon this error-ridden 64-page Village of Piermont financial report, when opining on the financial condition of the Village of Piermont? Of course, that becomes a non-issue, once I write to all of them simultaneously and tell them.

4. Has the New York State Comptroller's office (OSC) already relied upon this error-ridden 64-page Village of Piermont financial report when conducting their continuing Risk Assessment of shady Mayor Bruce Tucker's financial mishegoss and the Village of Piermont? Of course, this is already a non-issue, because you know that I already told them.

5. How many other certified public accountant audit reports are out there, that would slip-in a million-dollar “inadvertent reflection” on Page 47 of a 64-page audit report in the hopes that nobody catches it?

"Tucker and Associates"?...

GARBAGE and Associates.

5. How many other certified public accountant audit reports are out there, that would slip-in a million-dollar “inadvertent reflection” on Page 47 of a 64-page audit report in the hopes that nobody catches it?

"Tucker and Associates"?...

GARBAGE and Associates.